| Double-edged |

| Expediency |

| Crappiest company |

| Efficiency |

| Info you likely don't know |

| Technical oversights |

| Failures |

| Untruths |

| Londonism |

Click for DECEITFUL

|

| What should I do? |

The most important target is to declare total war on pollution. But metering is the next most important thing needed. This applies to tracking flows and losses in TW's own trunk mains and distribution networks. But let's concentrate on household supplies. Metering changes how most bill-payers use and value water.

Not all privatised water companies have behaved in the same way. Let's compare Thames Water's performance on metering with neighbouring water companies in the dry South and East of England. Even before privatisation, Southern Water (SW) opted for a policy of universal metering. Anglian Water (AW) also became progressive in metering.

Universal metering

Southern Water championed the concept of universal metering. Even before privatisation in 1989, the region had undertaken a major pilot in the Isle of Wight. This encountered both operational & political difficulties, with particular concern for the balance between external & internal meters, and fairness to families in receipt of income support. Yes, there's a social cost to metering. But there's a monster environmental & financial cost to not metering.Southern Water continued a progressive approach towards universal metering throughout their water-supply region. They gained experience. In a later phase they installed intelligent (Automated Meter Reading) meters that gave the company drive-by readings and logged leak alarms. If only their enterprise had been rewarded, enhanced and rolled out.

Of course, SW gained less income from metered customers who chose to cut back on their water use. But the company was doing the right thing: encouraging customers to attach a higher value to water. The policy radically reduced per capita consumption of water. Southern Water supplied less water in 2016 than they did in 1976. See Minutes 2:30 to 4:40 of this SW 2020 presentation on A resilient South East

.]

More than ten years ago, Ofwat published projections for 2014/15 for all Water Companies under the heading Properties billed and metering rates

. The Regulator projected that 92% of SW customers, 81% of Anglian Water and 37% of TW customers would be metered. So 63% of TW customers compared to 19% of Anglian Water and only 8% of SW customers were unmetered. Based on this snapshot, out of every 25 customers (i.e. bill-payers), only two of SW's were unmetered, fewer than five of AW's were unmetered but nearly 16 of TW's were unmetered. These figures demonstrate how shamefully late Thames Water was to prioritise metering.

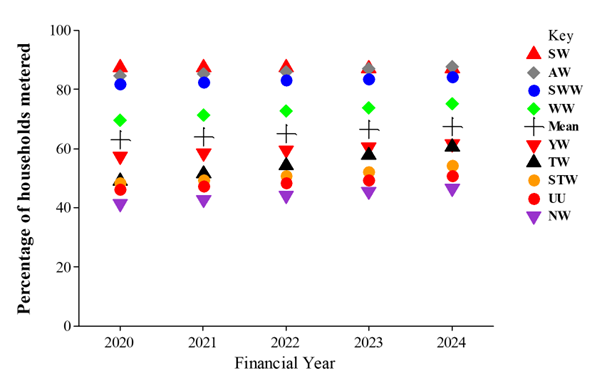

More up-to-date information is available via the Consumer Council for Water from which the comparison graph below derives. It shows the percentage of households metered for the nine Water and Sewerage Companies (WaSCs) principally operating in England:

|

Someone — presumably in Ofwat or Defra — decided that Thames Water and Anglian Water be designated early adopters of smart meters precisely because their regions are especially under stress for water resources. The selection of AW made sense but the selection of TW was very high-risk given the absence of a long culture of metering and of the strong customer engagement necessary to make it work well.

Parliamentary briefing paper CBP 7342, 27 June 2019, reports:

Thames Water is rolling out smart water meters to all its customers, starting in London. Thames Water says that installing smart meters is part of its plan

to protect water supplies for future generations, giving greater visibility and control to our customers to better understand and manage their water use.

The Thames Water smart meter roll-out began in London in 2015 and by March 2018 had installed 253,000 smart meters across fourteen London boroughs.

Press releases remain upbeat though futuristic.

TW implies that the company continues to install smart meters at the rate of about 80,000 per year. For some customers, the meters installed aren't fully smart yet and we aim to read these every six months.

I think we know what that means.

As ever, it's the effectiveness of the performance achieved & sustained that matters. Thames Water are throwing money at the problem with Arqiva, Honeywell, Sensus UK Ltd and Vodafone all involved. Have Morrisons (now part of M Group) been dropped?

Of critical importance will be the success of rolling out smart meters to previously unmetered customers. At a Utility Week Webinar in April 2024 on How to supercharge your smart metering success

, TW noted that the traditional water company business model is not set up to action what you find

from data insight (e.g. customer-side leakage). Southern Water have the systems and long experience. Clearly, Thames Water do not.

Mikal Willmott [leakage performance and strategy manager at Severn Trent] reviewing progress in Feb 2025 for CIWEM:

Smart meters will be pivotal in avoiding future water deficits, enhancing customer engagement and affordability — but they'll only be effective if supported by good governance

.In the eight years since Thames Water installed its first smart meter, the company's fleet of now more than a million meters have identified more than 80,000 leaks. This has saved 57 million litres of water a day, or enough to supply around 160,000 homes — the number projected to be served by the Havant Thicket Reservoir!

With 1,808,053 unmetered households to get round — 1,471,180 of them in London — the 80,000 per year rate of installation could take Thames Water over 22 years. The unmetered household numbers come directly from Table 3-1 of the Revised Draft Water Resources Management Plan (WRMP) 2024. You know, the WRMP on which Steve Reed — the then Secretary of State for Environment, Food and Rural Affairs — based his decision when greenlighting SESRO. The numbers of households quoted are for 2021-22.